3D Optimiser for Impact Funds

Thoughtfully incorporate impact funds into your portfolio allocation

Why a 3D Optimiser for Impact Funds?

Interest in impact investing is growing. Yet, investors typically allocate to impact funds independently from their traditional assets, foregoing diversification benefits. Since returns from impact funds correlate with traditional asset returns, taking such correlations into account allows for better portfolio diversification.

Our 3D Optimiser for Impact Funds brings together impact funds and traditional assets in an efficient portfolio allocation that maximises impact without financial sacrifice.

Access to this tool is restricted.

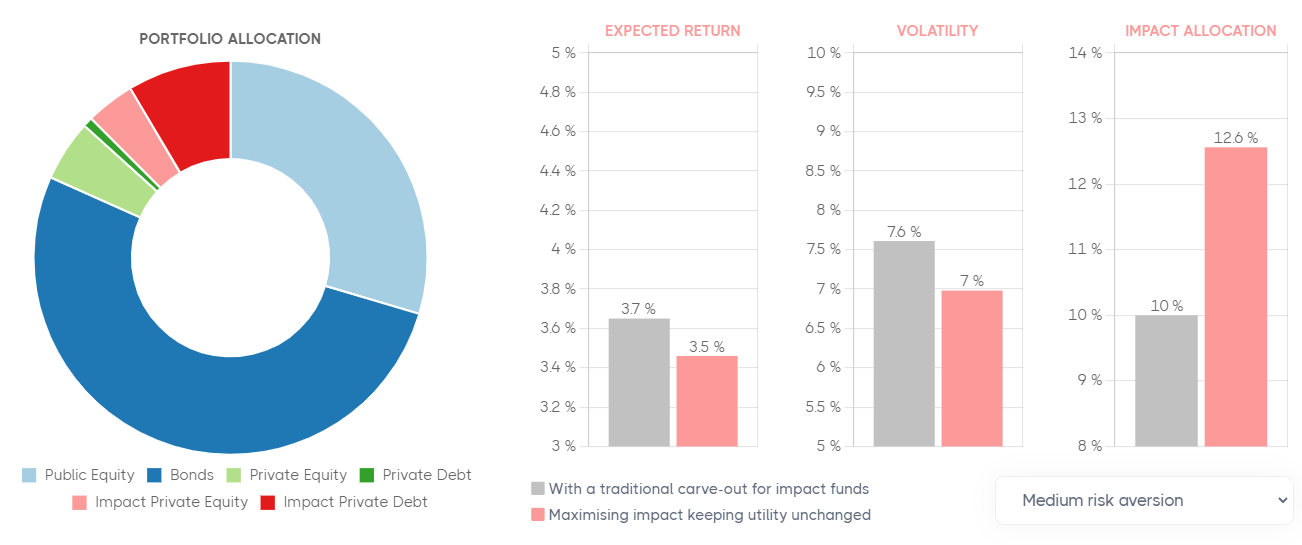

Typical results are pictured below.